Tax executives operate in a world where material transactions cannot wait for litigation to resolve interpretive uncertainty. The Internal Revenue Code is dense, dynamic, and increasingly shaped by subregulatory guidance and administrative interpretation.

Although litigation remains the ultimate backstop, most public companies, private equity sponsors, and closely held businesses cannot tolerate that level of uncertainty for transformational transactions. Issues can also surface years later—whether in an Internal Revenue Service exam or during due diligence for financing, investment, or a sale—where unresolved tax exposure can reduce valuation or jeopardize a transaction. Some owners wait for the IRS to initiate contact, but the risks and costs of uncertainty often grow over time.

Tools for certainty do exist. The question is when and how to use them. This article explores those tools in practical terms. Rather than providing abstract definitions, we frame the discussion as a series of conversations between a controversy-side practitioner (Pilar Puerto) and a transaction-side advisor (Ben Willis), highlighting how tax directors can design certainty in advance.

In practice, the mechanisms available to taxpayers fall along a continuum of certainty. At one end are informal discussions with the IRS and internal legal analyses prepared by tax advisors. At the other end are binding agreements with the government that conclusively resolve tax consequences for specific issues or periods. Between those poles lie several important tools that tax executives can use to manage uncertainty in material transactions.

This article explores four of the most significant mechanisms available today: closing agreements, prefiling agreements, private letter rulings, and formal tax opinions. Through a series of practical conversations between a controversy practitioner and a transactional tax advisor, we highlight how these tools operate, when they are most effective, and how tax directors can deploy them to reduce uncertainty before issues reach the examination stage.

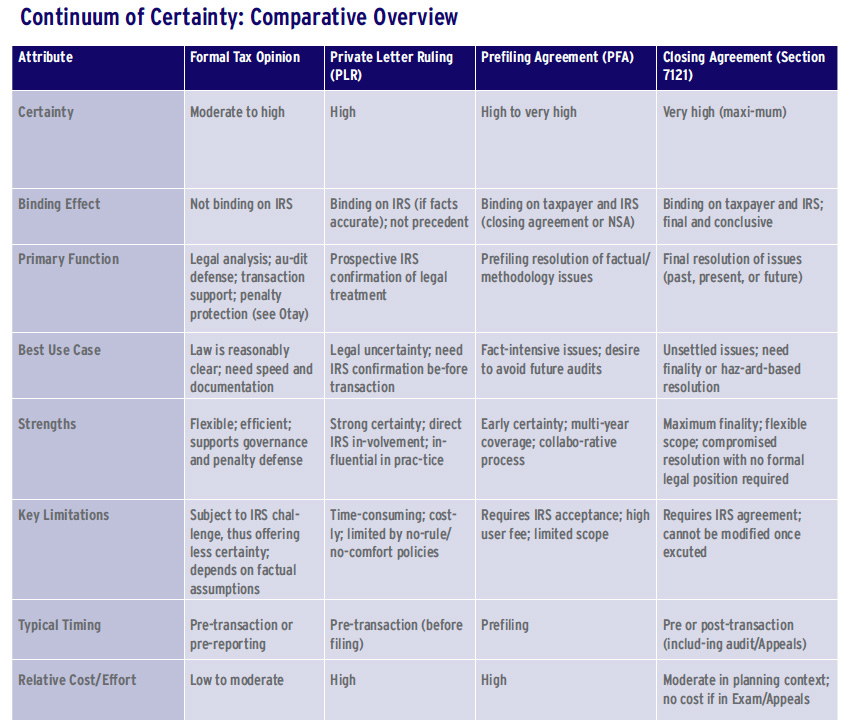

Continuum of Certainty

A useful way to frame these tools is along a continuum that pits certainty against cost, timing, and flexibility. At the end of least certainty are internal analyses and informal advice, which are fast and inexpensive but provide limited protection. Formal tax opinions increase confidence and may provide penalty protection but remain subject to challenge. Determination letters and private letter rulings introduce direct IRS involvement, offering greater certainty at the expense of time and cost. At the far end, prefiling agreements and closing agreements provide the most finality, binding both the taxpayer and the government, but also require the greatest degree of commitment.

In practice, sophisticated taxpayers do not view these tools in isolation. Instead, they design a strategy across this continuum, selecting the appropriate mechanisms according to the level of uncertainty, transaction timing, and risk tolerance.

Conversations With Pilar Puerto

“Pilar, What Is a Closing Agreement?”

A closing agreement under Section 7121 is the IRS’ most final and conclusive mechanism for resolving a taxpayer’s federal tax liabilities for specific issues or periods. A closing agreement is like a contract but is not strictly subject to contract law. For example, legal consideration is not required. The biggest difference from a contract is the closing agreement’s level of finality, which can make drafting one intimidating. Once executed, a closing agreement is binding on both the taxpayer and the government and may be reopened only under narrow circumstances such as fraud, malfeasance, or misrepresentation of material fact, a standard that courts interpret narrowly. Mere error is insufficient, as shown in Smith v. Commissioner, 159 TC 33 (2022) and the Internal Revenue Manual (IRM) 8.13.1.7.2(2).

Breadth and Flexibility

Section 7121 closing agreements are powerful and underused tools. The statute is drafted broadly. It does not limit the types of issues that may be resolved by a closing agreement, nor does it restrict the taxable periods covered. A closing agreement could cover multiple tax years, and multiple closing agreements could cover just one tax year. The regulations explicitly allow agreements to apply to periods ending after the date of execution, making closing agreements useful both for resolving past exposure and for providing forward‑looking certainty. Because the tool is narrow only in its finality, it can be deployed across a wide range of prelitigation contexts, preaudit, during examination, or at Appeals, saving time and resources for taxpayers and the IRS.

Practical Realities

Although powerful, closing agreements can be rare in practice, perhaps due to the lack of familiarity with them. They are used:

- during voluntary disclosure, before an audit;

- before a transaction or after a transaction before a tax return is filed;

- when factual or legal uncertainty makes finality more valuable than continued interpretive flexibility and a compromise is feasible;

- where a conventional audit adjustment cannot adequately or efficiently resolve the issue; and

- during long, drawn-out audits where the parties have come to an agreement as to some but not all issues.

National Office Closing Agreements

The IRS National Office may enter into a closing agreement either with or without issuing a private letter ruling (PLR), as shown in Revenue Procedure 2026‑1. Unlike PLRs, a National Office closing agreement does not require the IRS to articulate a legal analysis. The IRM instructs that these agreements should be “as brief and concise as possible,” as noted in IRM 8.13.1.4(3). This feature is especially useful when the law is unsettled or there is a hazards settlement, since closing agreements are made for disposing of debatable matters.

Compliance and Monetary‑Resolution Agreements

A closing agreement does not always require traditional tax adjustments. The IRS frequently uses compliance fee models to cure historical issues through a lump‑sum payment that makes the government whole. Examples include:

- Information reporting. IRM Exhibit 8.13.1‑1 provides a framework for voluntary settlements involving incorrect information reporting; and

- Method of accounting. Under Revenue Procedure 2002‑18, a taxpayer may avoid a method change and instead enter into a closing agreement that requires payment of a “specified amount” approximating the time value of money benefit of the prior method, adjusted for litigation hazards.

These approaches illustrate the flexibility of closing agreements for resolving imperfect fact patterns early and efficiently.

IRS Discretion and Governing Standard

The IRS has discretion to enter into a closing agreement. The regulations provide that an agreement may be used whenever there is an advantage in permanently and conclusively closing a matter, or when the taxpayer shows good and sufficient reasons and the government will not sustain a disadvantage. Importantly, the regulation does not require the IRS to obtain an affirmative benefit, only that it not sustain a disadvantage.

Comparison to Other IRS Resolution Tools

Closing agreements are particularly valuable when:

- the legal issue is unsettled, making prefiling agreements or PLRs (explained below) inappropriate;

- confidentiality matters, because closing agreements, unlike PLRs, are not subject to public disclosure;

- the ability to obtain a hazards settlement thereby does not require the IRS to take a firm legal position;

- certainty before a transaction is needed;

- final, conclusive, and efficient resolution of issues that can include past, current, and future years is available;

- a taxpayer seeks to voluntarily disclose issues and secure possibly more favorable terms before audit; or

- related account adjustments are impractical.

Closing agreements play a key role in appeals. Certain settlement structures are often implemented through closing agreements, such as mutual‑concession settlements (where litigation hazards are substantial on both sides) and split‑issue settlements (where full taxpayer or government wins are the only litigation outcomes).

Recent Developments: AIR Agreements

IRS guidance continues to encourage the use of closing agreements. The July 23, 2025, Interim Guidance Memorandum (LB&I‑04‑0725‑0008) clarifies that Accelerated Issue Resolution (AIR) agreements apply to cases in the Large Corporate Compliance program. The AIR program, established by Revenue Procedure 94‑67, allows taxpayers to voluntarily resolve recurring issues early when the IRS has already examined and resolved the same issues in prior years, minimizing repetitive audits. These issues are settled in closing agreements through this procedure. The memorandum encourages Exam teams to proactively identify issues suitable for AIR treatment.

Use of Closing Agreements vs. PLRs

From a strategic perspective, closing agreements occupy a unique position relative to private letter rulings. Whereas PLRs require the IRS to articulate a legal position when the government is comfortable doing so, closing agreements allow the parties to resolve uncertainty without requiring the parties to take a legal position (e.g., split issue settlements). This distinction becomes critical in cases involving unsettled law or hazards of litigation.

In those situations, taxpayers could find that a closing agreement may be not only faster but also more achievable than a PLR.

“What Is a Prefiling Agreement?”

The IRS’ Pre-filing Agreement (PFA, their spelling) program allows taxpayers to work with the IRS to resolve specific issues before they file a return. In essence, the PFA functions as a focused, prefiling examination designed to eliminate later controversy. This program benefits both taxpayers and the IRS, because a prefiling examination allows for more timely access to relevant records and personnel. It also provides taxpayers certainty for multiple years.

PFAs are not PLRs or litigation settlements. A PFA is a collaborative issue‑resolution tool aimed at promoting certainty generally on the determination of facts, the application of well-established principles to known facts, or the methodology a taxpayer will use to determine an amount of income, allowance, deduction, or credit.

Structure and Effect of PFAs

A PFA may take one of two forms:

- closing agreements under Section 7121 used for the current taxable year or any prior taxable year for which a return is not yet due; or

- non‑statutory agreements (NSAs) used for the current taxable year, any prior taxable year for which a return is not yet due, and up to four future taxable years.

Once executed, both forms bind the taxpayer and the government.

Closing agreements may be reopened only in cases of fraud, malfeasance, or misrepresentation of material fact as we discussed. NSA PFAs are similarly conclusive but allow modification or termination by mutual consent. They may also incorporate stated assumptions such as future conditions (for example, industry factors or business operations) that must remain true for the agreement to remain in effect. If a stated assumption ceases to hold, the agreement terminates at the start of that taxable year. This ability to use stated assumptions provides flexibility for issues spanning multiple future years.

Access and Fees

Taxpayers must apply for acceptance into the program. Because PFAs require significant IRS resources, a user fee applies, $181,500 in 2026, as set annually in the “‑1” annual Revenue Procedure.

In recent years, the IRS has focused on expanding and improving the program. Coverage expansions include the ability to address future years and, under Revenue Procedure 2016‑30, a broadened scope that now covers issues regarding certain method‑of‑accounting changes. In 2025, the IRS revamped the PFA website, which now features:

- a dedicated page describing likely suitable issues and required documentation;

- guidance on timing to help taxpayers align PFA submissions with filing deadlines and transactions; and

- updated step-by-step submission instructions with timing expectations.

The inclusion of the PFA revenue procedure in the IRS Priority Guidance Plan underscores continued agency commitment to the program.

Practical Considerations for Tax Directors

PFAs are particularly valuable when:

- the issues require factual determination or the application of well-established legal principles

to facts; - the taxpayer seeks agreement on a methodology (for example, identifying qualified research expenses under Section 41);

- early engagement is feasible, because applications must be submitted before the relevant return is filed; and

- the relevant transactions are complete.

From FY2019 through FY2025, nearly half of all PFA submissions involved the research credit or the Section 165(g)(3) worthless stock deduction. Other requests addressed issues such as sale‑leaseback structures, the characterization of loans for federal tax purposes, pass-through elections, and whether a trust qualifies as a US person. PFAs are generally not appropriate for:

- matters already in a litigation posture;

- issues for which the taxpayer has already requested a PLR or closing agreement;

- instances when a PFA would conflict with existing IRS determinations;

- issues without well-established law; and

- issues explicitly excluded under Revenue Procedure 2016‑30, including penalties, Section 482 transfer pricing issues, and other ineligible items.

“What Is a Non-Statutory Agreement?”

For purposes of this article, it is important to briefly discuss settlement agreements that the IRS routinely enters into and point out the difference between these settlement agreements and closing agreements. These settlement agreements are non‑statutory agreements, which are agreements the IRS enters into outside the authority of specific statutes such as Section 7121 (closing agreements) and Section 7122 (offers in compromise). Examination and Appeals routinely use these agreements to memorialize adjustments or to waive restrictions on assessment. Common examples include:

- Form 4549. Income Tax Examination Changes;

- Form 870. Waiver of Restrictions on Assessment and Collection of Deficiency in Tax and Acceptance of Overassessment; and

- Form 870‑AD. Offer to Waive Restrictions on Assessment and Collection of Deficiency in Tax and to Accept Overassessment.

Although widely used, these documents lack the finality of a closing agreement. The IRS recognizes this difference; for example, IRM 8.6.4.4.3 instructs IRS personnel to first seek Form 870‑type agreements, then Form 870‑AD agreements, and to use a closing agreement only when the taxpayer insists on greater finality and the government would not sustain a disadvantage by doing so.

Courts have consistently held that agreements that do not satisfy the strict requirements of Section 7121, such as Form 4549 and Form 870-AD, lack the finality of a closing agreement.1 These forms may document an agreed-upon adjustment, but they may not prevent the IRS from revisiting an issue when legally permissible. This lack of finality, however, could favor a taxpayer that, for example, wants to file a refund claim for a retroactive change in the applicable statute.2 Exam and Appeals also make these tools readily available. Their use, however, is more limited than a closing agreement that is wide in scope but narrow in finality.

Conversations With Ben Willis

“Ben, What Is a Private Letter Ruling?”

A PLR is the IRS’ most direct mechanism for providing taxpayer-specific prospective guidance on the federal tax consequences of a proposed transaction. A PLR represents the IRS National Office’s formal interpretation of how the Internal Revenue Code applies to a specific set of facts presented by the requesting taxpayer. The PLR is binding only if the facts are exactly as represented and will not protect the taxpayer if they differ during later examination.

PLRs are issued according to the IRS’ administrative authority to provide written determinations to taxpayers seeking clarity on the application of federal tax law. The IRS has long maintained that issuing rulings “whenever appropriate in the interest of sound tax administration” promotes voluntary compliance and improves relations between taxpayers and the government.

A ruling binds the IRS with respect to the requesting taxpayer if the transaction is carried out as described in the ruling request. However, PLRs do not constitute precedent, and other taxpayers cannot rely upon them. Instead, they function as a transaction-specific commitment by the IRS regarding the tax consequences of the particular facts presented. Note that the IRS is bound in court by the rulings in a PLR, whereas a taxpayer is not. This further means that the IRS is bound to the ruling with regard to the specific requesting taxpayer, even if another taxpayer to the same transaction takes a different position.

Although PLRs lack authority as precedents, they are nevertheless highly influential in practice. Because ruling requests require taxpayers to present detailed factual representations and legal analysis, the process often raises issues that might otherwise lead to controversy during examination.

For many complex transactions, particularly tax-free reorganizations, divisive transactions, or cross-border restructurings, a ruling can serve as the most authoritative method to eliminate interpretive uncertainty prior to execution.

“When Should You Seek a PLR?”

A PLR is generally appropriate when a transaction involves novel legal questions, ambiguous statutory interpretation, or significant financial consequences if the tax treatment were later challenged. The IRS typically considers ruling requests where:

- the issue turns on statutory interpretation rather than on factual determinations;

- the transaction has significant tax consequences (although comfort rulings are back in effect); and

- the taxpayer requires certainty before executing the transaction, although certainty exists only if the facts turn out to be exactly as represented.

In practice, ruling requests frequently arise in areas such as:

- corporate liquidations, incorporations, spin-offs, and reorganizations under Sections 332, 351, 355 and 368, respectively;

- consolidated return issues under Treasury Regulations Section 1.1502;

- cross-border transactions governed by Section 367 or Section 7874;

- entity classification and accounting method changes; and

- certain estate, gift, or employee benefit determinations.

From a procedural perspective, the taxpayer submits the ruling request to the Office of Chief Counsel and must include a full description of the transaction, representations of fact, and a legal analysis supporting the requested conclusion. The IRS typically conducts an initial review and will contact the taxpayer within approximately twenty-one days if additional information is required.

However, obtaining a ruling can be expensive and time-consuming. User fees alone typically reach almost $45,000 for larger taxpayers (and over six figures for those in the Advance Pricing Agreement or APA program), and the process may require months of interaction with the National Office. As a result, taxpayers must balance the value of certainty against the cost and timing of applying for a ruling. Small taxpayers, including corporations with less than $10 million in gross receipts, can qualify for reduced fees.

“How Do the No-Rule List and the ‘No-Comfort’ Ruling Policy Differ?”

Two threshold limitations govern access to the PLR process: 1) the IRS’ “no-rule” list and 2) the IRS’ “no-comfort” ruling policy.

First, a PLR will not be issued if the relevant matter appears on the IRS’ published “no-rule” list. Revenue Procedure 2026-3 details the areas in which the IRS has determined, as a matter of administrative policy, that rulings are inappropriate. Tracking stock, reflecting economic ownership, is a good example that falls exclusively to tax opinions.

Second, even when an issue does not appear on the no-rule list, the IRS generally will not issue so-called “comfort rulings.” Under this policy, the IRS declines to rule on issues that are clearly and adequately addressed by existing authorities, including the Internal Revenue Code, Treasury regulations, judicial decisions, revenue rulings, revenue procedures, and other published guidance. In such cases, the IRS expects taxpayers to rely on existing law rather than to seek confirmation through the ruling process.

Notwithstanding this general policy, the IRS has carved out important exceptions for certain corporate transactions. Even when relevant law is well-developed, the IRS will issue PLRs addressing the qualification of transactions under the following provisions: Section 332 (tax-free liquidations), Section 351 (tax-free incorporations), Section 355 (tax-free spin-offs), Section 368 (tax-free reorganizations), and Section 1036 (certain stock-for-stock exchanges). Of course, step transaction, substance over form, and economic substance penalties are especially relevant when addressing these exceptions to gain recognition.

The exceptions reflect the significance and complexity of these transactions, as well as the practical need for transactional certainty in high-value corporate restructurings.

Other IRS Procedures Relevant to the PLR Framework

Several additional IRS programs provide guidance or relief in contexts adjacent to the PLR process. Although beyond the scope of this discussion, they are important in determining when a PLR is appropriate.

As a general rule, taxpayers must request a PLR in writing before filing the relevant return. (See Revenue Procedure 2026-1, Section 2.01.) The following mechanisms, in contrast, often apply after a transaction has occurred or in the context of an examination:

- Section 9100 relief (late elections). The “9100” ruling process provides relief for taxpayers who fail to make timely regulatory elections. Unlike traditional PLRs, these rulings are frequently requested—and granted—after the relevant transaction has been completed and the return filed;

- Technical advice memoranda (TAMs). TAMs are written determinations issued by the IRS National Office in response to requests from field exam teams. They address the application of law to specific facts arising during an audit. Taxpayers may participate in the process, but unlike with PLRs, taxpayers cannot initiate TAMs;

- Determination letters. IRS field offices rather than the National Office issue determination letters, which apply to specific categories of issues assigned to those offices. For example, certain consolidated return matters, such as failures relating to Form 1122 under Treasury Regulations Section 1.1502-75(b), are resolved through the determination letter process rather than through PLRs; and

- The Advance Pricing and Mutual Agreement (APMA) program (formerly the APA program). The APMA program provides prospective certainty for transfer pricing by establishing agreed-upon methodologies for cross-border transactions. Although distinct from the PLR process, it similarly reflects a preemptive approach to resolving tax uncertainty.

“When Is a Tax Opinion Enough?”

Whereas PLRs represent a higher level of administrative certainty available before litigation, most transactions rely instead on tax opinions issued by counsel.

A tax opinion is a formal legal analysis evaluating the likelihood that a particular tax treatment would be sustained if challenged. Opinions typically range across a spectrum of confidence levels, including conclusions such as “more likely than not,” “should,” and “will.” The level selected depends on the strength of the supporting authorities and the purpose the opinion is intended to serve, as we’ll see.

Tax opinions have several important functions in practice. First, they provide technical assurance to management and boards of directors that the expected tax consequences of a transaction are defensible. In complex corporate transactions, directors often rely on expert advice to satisfy their fiduciary duty of care when approving tax-sensitive structures.

Second, opinions frequently serve as conditions to closing in mergers and acquisitions, particularly where the parties intend the transaction to qualify as a tax-free reorganization under Section 368.

Third, opinions may protect against penalties under the Internal Revenue Code. A properly reasoned opinion concluding that a position is “more likely than not” correct may support a taxpayer’s defense against certain penalties for inaccuracies.

In many cases, therefore, a carefully prepared tax opinion provides sufficient comfort without the expense and delay associated with requesting a ruling from the National Office.

In large corporate transactions, tax opinions frequently function as the practical foundation for tax certainty. Transactions involving significant built-in gain, such as divisive reorganizations under Section 355, reorganizations under Section 368, or cross-border restructurings, often depend on opinion letters confirming that the intended tax treatment is likely to withstand a challenge.

In practice, opinion levels correspond to different technical thresholds. For return reporting purposes, taxpayers may rely on positions supported by “substantial authority” without filing a disclosure under Form 8275. A “more likely than not” opinion is often the relevant standard for financial statement reporting and audit defense. Higher-confidence conclusions—such as “should” or “will”—are sometimes required in regulated transactions or where contractual certainty is particularly important.

These opinions serve not only as technical analysis but also as governance tools. Boards of directors and transaction committees frequently rely on formal opinion letters when approving tax-sensitive transactions involving substantial economic value.

Opinions are particularly common when obtaining a PLR is impractical due to timing or cost. In mergers and acquisitions, for example, delivery of a tax opinion is often a condition for closing when the parties intend the transaction to qualify as a tax-free reorganization. In other situations, opinions help demonstrate that the taxpayer reasonably relied on competent professional advice when adopting a particular tax position.

Opinion Thresholds and Penalty Protection

It is also important to distinguish between opinion thresholds and their practical implications. Whereas “substantial authority” may be sufficient to avoid disclosure penalties in certain cases, a “more likely than not” opinion is typically the relevant benchmark for penalty protection under Section 6662 and for financial reporting. Higher levels of comfort—such as “should” or “will”—are generally driven by transactional requirements, such as closing conditions or board-level governance expectations.

Recent Tax Court authority reinforces this point: in Otay Project LP v. Commissioner, TC Memo 2026-21 (February 23, 2026), the court held that well-developed tax opinions, grounded in “relevant provisions of the Code, Treasury regulations, published Internal Revenue Service rulings, and judicial decisions” and reflecting a thorough understanding of the taxpayer’s facts, can satisfy the reasonable basis standard and provide meaningful protection against penalties, even when the IRS ultimately prevails on the underlying issue.

As a result, the decision to obtain an opinion is not merely technical. It also reflects a broader risk management determination regarding audit exposure, financial statement impact, and stakeholder expectations.

“How Do PLRs and Opinions Interact?”

Rather than representing competing tools, PLRs and tax opinions exist along a continuum of certainty available to taxpayers.

At one end of the spectrum are internal analyses and informal advice from tax advisors. Formal written opinions provide a higher level of confidence by articulating the legal authorities supporting the anticipated tax result.

Beyond that level sits the PLR, which offers a taxpayer-specific administrative commitment from the IRS itself.

“What Tool Should I Use?”

From a strategic perspective, practitioners often view these tools as complementary:

- opinions are appropriate when the law is reasonably clear and the primary objective is to document the strength of the position (as well as when speed matters);

- PLRs are preferable when the law is uncertain and the taxpayer seeks IRS confirmation before proceeding;

- closing agreements are preferable to obtain certainty in a tax position for past or future years and the law is uncertain. Closing agreements can involve prospective transactions. This is the most flexible but also the most final option; and

- PFAs are preferable when the issue is fact-intensive and the personnel and documentation are more readily available in the present. The taxpayer can obtain certainty for future years, avoiding costly audits concerning the same issue. PFAs cannot involve issues attached to prospective transactions. The amount at stake, though, should justify the substantial fee.

In practice, sophisticated taxpayers frequently combine these approaches. Tax practitioners may first develop a legal opinion analyzing the transaction or position and then use that analysis as the foundation for a request for a ruling or closing agreement. The opinion framework often shapes the IRS discussion during the ruling or closing agreement process. On other issues or once a transaction has already occurred, a taxpayer’s counsel may decide to go the PFA route when the law is already well settled.

Ultimately, the choice to seek an opinion, a PLR, or another certainty-enhancing mechanism such as a closing agreement or a PFA is a strategic one. The correct approach depends on the materiality of the issue, the level of uncertainty in the law, the timing of the transaction or related event, and the taxpayer’s tolerance for risk.

Benjamin M. Willis is managing director, corporate and transactional tax, at Baker Tilly US, LLP. Pilar Puerto is a partner at Dinsmore & Shohl LLP.

Endnotes

- Botany Worsted Mills v. United States, 278 U.S. 282, 289 (1929); Whitney v. United States, 826 F.2d 896, 896 (9th Cir. 1987); Hudock v. Commissioner, 65 T.C. 351, 354–355 (1975); Holland v. Commissioner, 70 T.C. 1046 (1978) aff’d., 622 F.2d 95 (4th Cir. 1980); Goldberg v. Comm’r, T.C. Memo. 2020-38 (2020).

- Guggenheim v. United States, 77 F. Supp. 186 (Ct. Cl. 1948), cert. denied, 335 U.S. 908 (1949).